At Achieve, we're committed to providing you with the most accurate, relevant and helpful financial information. While some of our content may include references to products or services we offer, our editorial integrity ensures that our experts’ opinions aren’t influenced by compensation.

Achieve Insights

Improving financial health is about more than FICO Scores

Mar 19, 2024

Reviewed by

How do we help struggling Americans return to financial health and begin working toward more aspirational financial goals? First, we have to look beyond the FICO.

Recently, the average U.S. FICO Score fell for the first time in a decade. Granted, the decline was just a single point, to 717, but the immediate commentary that followed was that this development is an early indicator that the ongoing effects of high interest rates and inflation are having on consumers' financial health, especially among those already struggling. Everywhere you look — news headlines, grocery store prices, the bills at the end of the month — prices are up and financial health, or that simple feeling of “getting by,” is becoming increasingly more difficult to attain.

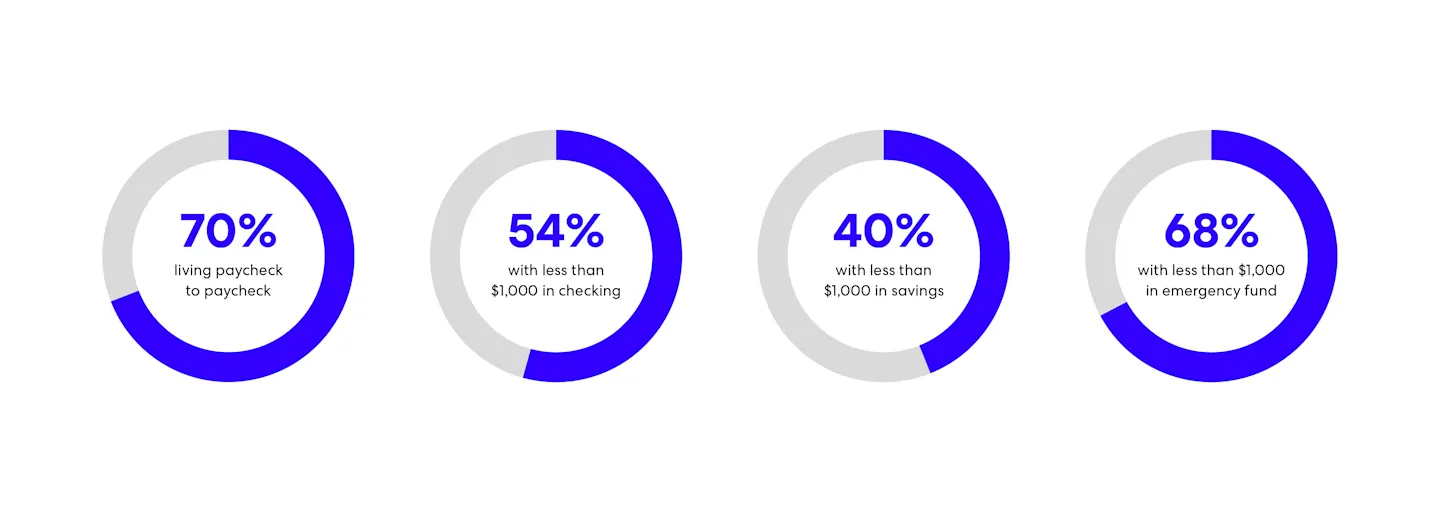

Our recent survey painted a similar picture. Achieve Center for Consumer Insights data showed that 80% of Americans surveyed felt that their expenses were tracking at similar or increased levels to the year before, with only 20% seeing a decrease in expenses year over year. Over 70% reported living paycheck-to-paycheck. 54% of those surveyed reported having less than $1000 in their checking account, 40% reported having less than $1,000 in their savings account and a whopping 68% reported having less than $1,000 in an emergency savings fund. Of those surveyed, 49% listed their credit score as being below 739 (Good) with an additional 14% unaware of their current credit score.

The impact of this “paycheck-to-paycheck” mentality is shifting long-term aspirations with far fewer Americans striving for the financial goal of becoming “rich” and far more pivoting to just trying to be able to pay their bills on time. The survey asked consumers to select the ideas of financial freedom that they most agreed with and found the most common definitions were:

— Living debt free: 54%

— Living comfortably, but not necessarily being rich: 50%

— The ability to regularly meet all of their financial obligations and still have some money left over each month: 49%

— Never having to worry about money: 46%

Surprisingly, the survey also found that far fewer respondents believe financial freedom means being rich (12%) or having enough money to give up working altogether (32%).

So, how do we help struggling Americans return to financial health and begin working toward more aspirational financial goals? First, we have to look beyond the FICO.

According to industry leader Financial Health Network, a more holistic framework should be used to assess financial health. The framework outlines four key categories:

Spend: Spend less than income and pay bills on time

Save: Have sufficient liquid savings and have sufficient long-term savings

Borrow: Have manageable debt and have a prime credit score

Plan: Have appropriate insurance and plan ahead financially

But how do we focus on the future if our status today is still in flux? Here are four simple steps to take digestible financial bites toward financial freedom:

1. Start with a budget that is based on a realistic picture of income and expenses: First, understand what comes in and what goes out each month. You can do this with pen and paper, in a spreadsheet, or using an easy money management app. Add up all your income, including wages, side hustles, gig work, alimony and child support. Next, look at where that money goes, and categorize your expenses into fixed (things like mortgage, rent, car insurance, cell phone or childcare), variable (utilities, gas or groceries) and discretionary (dinners out, gifts, shopping or other entertainment).

2. Create an Envelope Budget for discretionary spend: Envelope budgeting can be a great way to pre-plan where your money is going each month to insure you aren’t over spending, you’re paying bills on time and you’re looking at opportunities to slash budget items that might be creating overages. Create an envelope for Savings, even if you can only allocate a few dollars each month.

3. Deal with debt: If you have credit card debt, medical debt, personal loans, or other debts, make a plan for knocking them down. The reason debt should be a priority is that it’s costly. The longer you wait to get a handle on debt, the more interest you’ll pay. That takes away dollars that could be directed to your financial goals. Minimum payments won't cut it, especially if you're stuck with double-digital APRs. If you have a credit card with a $10,000 balance and a 24% APR and you make only the required minimum payment each month, it’ll take you almost 30 years to pay off the debt and you’ll pay more than $19,000 in interest. If you’ve got debt and you’d like to get rid of it, explore debt solutions to figure out which strategy is right for your situation.

4. Shout your budget loud and proud: Keeping your budget and financial concerns to yourself is on the outs. Instead, focus on “loud budgeting,” demystifying conversations about debt and budgeting with no stigma attached. This way it makes it easier to decline that pricey dinner out or weekend away with friends so you can stay focused on growing your savings, shrinking your debt and moving your financial future forward.

Author Information

Written by

Vice President, Corporate Communications

Reviewed by

Analyst, Achieve Center for Consumer Insights

Related Articles

Americans in their 20s and 30s are becoming seriously delinquent on their credit cards at a faster pace than before the pandemic and approaching levels not seen since the Great Recession.

On the surface, the premise of Buy Now, Pay Later is simple and appealing. But borrowers who can’t afford to repay their BNPL loans risk getting hit with late fees, falling behind on other financial obligations, damaging their credit and other challenges.

With financial volatility on the rise, it’s time to rethink how people use mobile apps to manage their money

Americans in their 20s and 30s are becoming seriously delinquent on their credit cards at a faster pace than before the pandemic and approaching levels not seen since the Great Recession.

On the surface, the premise of Buy Now, Pay Later is simple and appealing. But borrowers who can’t afford to repay their BNPL loans risk getting hit with late fees, falling behind on other financial obligations, damaging their credit and other challenges.

With financial volatility on the rise, it’s time to rethink how people use mobile apps to manage their money