At Achieve, we're committed to providing you with the most accurate, relevant and helpful financial information. While some of our content may include references to products or services we offer, our editorial integrity ensures that our experts’ opinions aren’t influenced by compensation.

Personal Loans

Prequalification vs. preapproval

Feb 12, 2026

Reviewed by

Key takeaways:

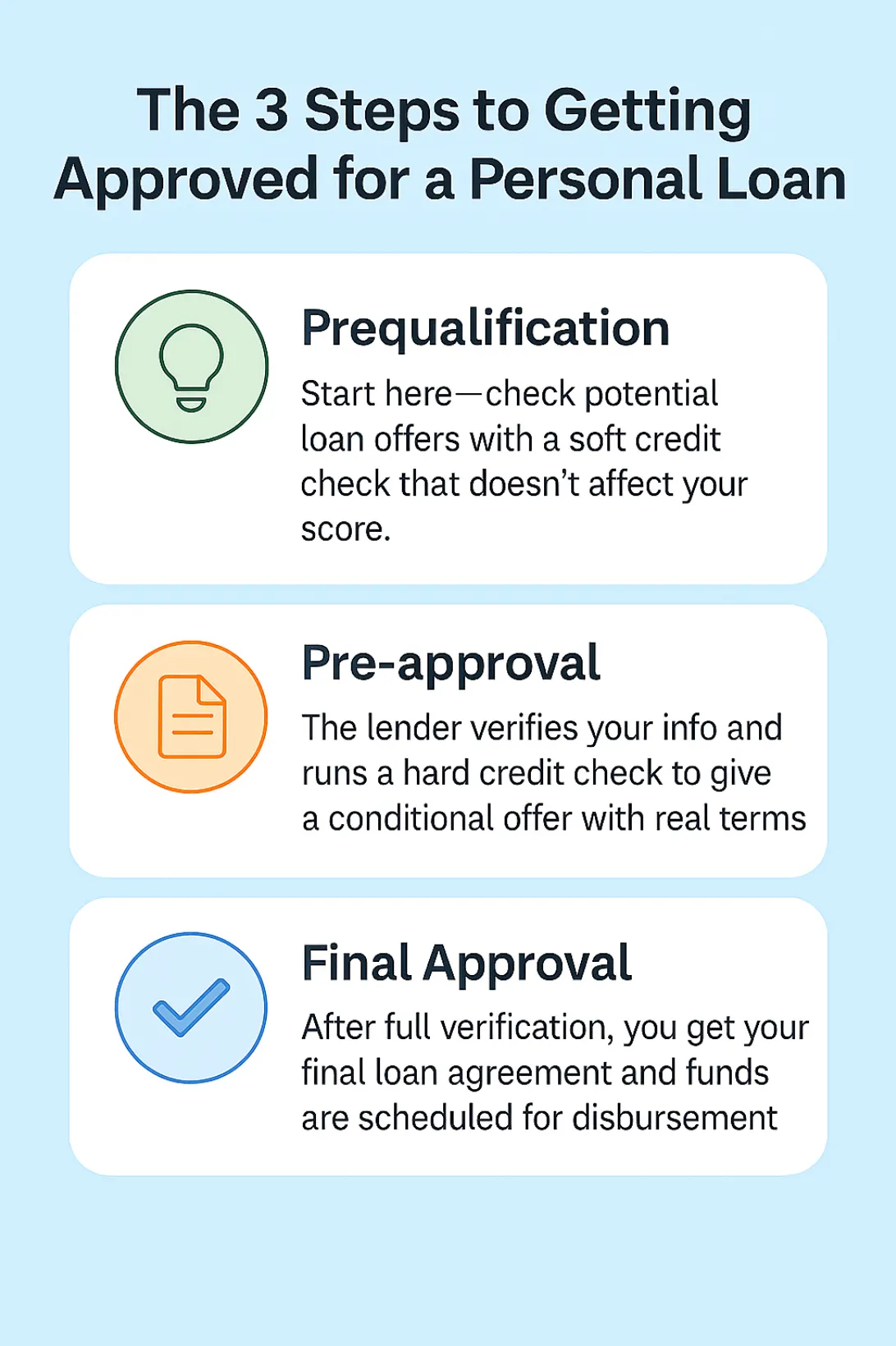

During prequalification, you provide a lender with basic information about yourself and your finances, and the lender does a soft pull on your credit report. This doesn’t impact your credit score.

During preapproval, you provide a lender with more detailed information about your financial situation, and the lender does a hard pull on your credit report. Although the hard pull may not drop your credit score much, the impact of multiple hard pulls could add up.

After several months of on-time loan payments, your score is likely to rebound.

You’ve decided to apply for a loan, and you’re anxious to move forward. You understand what APR means, have a good idea of what documents you need, and you’ve worked a new monthly payment into your budget. The only remaining question is whether you should be looking for prequalification or pre-approval.

While the two terms are similar, they represent different parts of the loan process. By the time you’re done reading, you’ll understand the difference between prequalification and preapproval, and find out if either one hurts your credit score.

What does prequalification mean?

Prequalification is a less-formal assessment of your credit, based entirely on self-reported financial information. In other words, when you prequalify for a personal loan, you don’t have to supply any documents to back up the answers you provide on a prequalification application.

Usually, you fill out a short application providing the lender with basic information such as your name, Social Security number, contact information, income, and outstanding debts. Based on the information you provide, the lender lets you know if it believes you’re a good candidate for a loan. If so, the lender tells you how much you could potentially borrow, what your interest rate may be, and any fees associated with the loan.

Prequalification can be a good indicator that you'll be approved if you apply, but it's not a guarantee. On the other hand, being denied prequalification for a loan is a strong indicator that you should look for another lender.

No impact on your credit score

When you’re prequalifying for a personal loan, the lender conducts a soft pull or soft inquiry on your credit report. While a soft pull doesn’t provide the same level of detail as a hard pull, it offers the lender a sense of whether you’d be a good candidate for a loan.

With a soft pull, the lender can see the following information:

Personal information such as your name, date of birth, and home address

Current credit agreements (who you’re currently borrowing from)

Recent financial history such as missed payments or bankruptcies

Your credit score or credit score range.

Soft pulls are conducted for all types of loans, including personal loans, auto loans, and home equity lines of credit (HELOCs). Credit card companies also use them for pre-screened credit offers, and potential employers sometimes conduct soft credit pulls on job applicants—particularly if the job involves dealing with money.

You usually don’t have to sit around wondering whether you prequalify for a personal loan, as most soft pulls are completed in a matter of minutes. You also won’t have to worry about the impact of a soft pull on your credit score because finding out if you prequalify for a loan doesn't hurt your credit.

Comparing apples to apples

It’s worthwhile to shop around for a loan, and since soft credit pulls don’t hurt your credit score, you can check with multiple lenders before deciding which to work with.

Remember, once you complete the prequalification process, the lender provides you with basic information such as how much you might borrow, the potential interest rate on your loan, and any associated fees. So shopping around allows you to compare loan offers apples to apples.

What does preapproval mean?

Getting preapproval for a personal loan means you’re almost, but not quite done with the application process. It’s a more detailed look at your finances, this time with a hard credit inquiry that will probably drop your credit score a little.

The difference between prequalified and preapproved is that once you’re preapproved, the lender is basically saying that if everything checks out, you’re probably good to go with the loan.

Be prepared to offer the following information and application documentation:

Photo ID, like a driver’s license or passport

Proof of home address, such as a mortgage statement, rental agreement, or utility bill

The name and address of your employer(s) going back two years

Proof of income, such as recent pay stubs, W-2, or your tax return

Your bank account number

Your latest bank statement

Although you may not be asked for all these documents, gathering them in advance means you can provide them to the lender quickly when requested.

Impact on your credit score

After you’ve decided which lender to work with, the lender asks you to fill out a complete, in-depth loan application for preapproval. This application goes into more detail, and may require documentation.

It’s during this part of the process that a lender conducts a hard pull (or hard inquiry). A hard pull could impact your credit score, although it’s not dramatic (usually a drop of 10 points or less). Fortunately, it should quickly rebound with regular on-time monthly payments.

Loan preapproval could be near-instant, or it could take one to three business days—it all depends on the lender. Like prequalification, being preapproved for a loan is a good sign but it’s not a guarantee of a loan.

What happens after preapproval?

You’re nearly there. All that’s left to do is to send your loan through underwriting. Underwriting means verifying the information you’ve provided so the lender can be sure loaning to you is a safe bet—basically, that they believe you can handle the payments. For example, the underwriter may check whether anything has changed since you filled out the application, such as a job loss or a change in your credit profile.

Don’t worry if the lender asks you to provide additional documentation—it’s just due diligence. For example, if you’re self-employed or paid on commission, you may be asked to give a bit more financial information. It’s all a normal part of the process.

How long the underwriting process takes varies depending on the type of loan (a mortgage typically takes longer than a personal loan approval) and the kind of underwriting used (automated, manual, or a bit of both).

Once the loan application makes it through underwriting, you should receive final approval so long as nothing major has changed.

Which one should you do first?

Here’s the sequence your loan process should follow:

Shop for a loan: Check with at least three lenders (more is better) to compare loan offers.

Prequalification: This step saves you the time and trouble of applying for the loan if the lender doesn't believe your application will make it through underwriting. And because the lender uses a soft pull, there's no impact on your credit score.

Preapproval: Preapproval is your chance to lay it all out for the lender, showing that you can afford and handle the loan.

Final approval: Once you receive final approval, it's time to sign your loan contract and discuss how the proceeds will be disbursed.

What happens after final approval?

The lender provides you with a loan contract you should carefully read over before signing. Depending on where your lender is, you may pick up the check in person, have it mailed to you, or have the funds deposited in your bank account.

If you’re anxious for the money (and who’s not?), you can do some things that may speed the loan process along. Double-check your loan application before submitting it to ensure all information is correct, and gather any documents you’re likely to need in advance so they’re ready to go when requested.

All that’s left to do is shop for a loan that fits your goals and budget. Once you’ve found the right lender, it’s time to get started on that loan application.

Ready to get started? Check your rates with Achieve Personal Loans without hurting your credit score.

Author Information

Written by

Dana is an Achieve writer. She has been covering breaking financial news for nearly 30 years and is most interested in how financial news impacts everyday people. Dana is a personal loan, insurance, and brokerage expert for The Motley Fool.

Reviewed by

James is a financial editor for Achieve. He has been an editor for The Ascent (The Motley Fool) and was the arts editor at The Valley Advocate newspaper in Western Massachusetts for many years. He holds an MFA from the University of Massachusetts Amherst and an MA from Hollins University. His book Krakatoa Picnic came out in 2017.

FAQs: Prequalification vs. preapproval

No. Since the lender conducts a soft credit check during the prequalification process, there’s no impact on your score.

Yes. If key details change, the loan could be denied. Let’s say you go into work the day after applying for a loan and learn that your company is closing. That key change could impact your ability to repay the loan and might lead to a denial of your application.

If you’re unsure you’re ready to sign for the loan, ask the lender how long your preapproval will last. Typically, it’s 30-60 days.

Related Articles

Learn how unsecured personal loans work, compare rates and terms to credit cards, and find out how to qualify — even with fair credit. Apply today.

Adding a co-signer to a personal loan application could improve your approval odds and rate. Learn what lenders look for and how to apply with Achieve.

Obliterate your high interest credit card debt with a low interest personal loan and get out of debt faster. Our expert tells you how.

Learn how unsecured personal loans work, compare rates and terms to credit cards, and find out how to qualify — even with fair credit. Apply today.

Adding a co-signer to a personal loan application could improve your approval odds and rate. Learn what lenders look for and how to apply with Achieve.

Obliterate your high interest credit card debt with a low interest personal loan and get out of debt faster. Our expert tells you how.